State Tax Reciprocity Agreements (2026)

When an employee lives in one state and works in another, payroll withholding can get messy fast. The good news: some states have reciprocity agreements that let employees pay state income tax only to their state of residence, while the work state waives income tax withholding on wages.

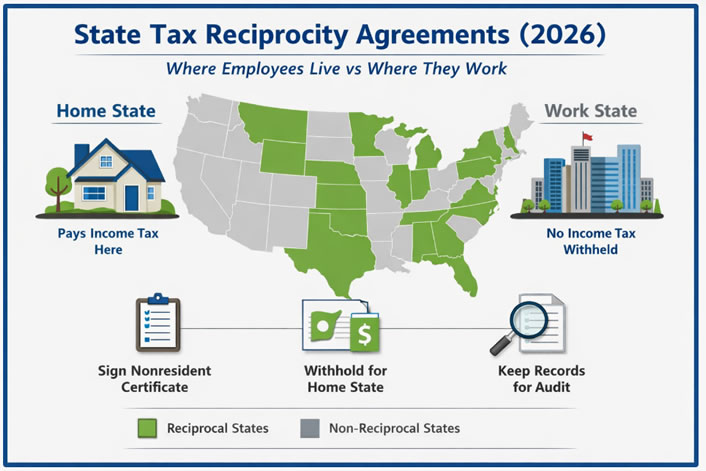

This guide shows the reciprocity states in 2026, the nonresident certificate forms employees typically must sign, and a payroll-ready workflow you can plug into your multi-state process.

Important: Reciprocity generally applies to state income tax withholding only. It typically does not change unemployment tax (SUI), which usually follows where the employee works.

What is a state tax reciprocity agreement

A reciprocity agreement is an arrangement between two states (or a state and DC) that allows a commuting employee to request exemption from income tax withholding in the work state, so the employer withholds only for the home state.

If there is no reciprocity, employees often file a nonresident return in the work state and a resident return in the home state, typically using a credit for taxes paid to another state to reduce double taxation.

How reciprocity works in payroll

- Employee action: the employee signs a nonresident certificate (or equivalent) and gives it to the employer.

- Employer action: the employer withholds state income tax for the home state instead of the work state.

- Recordkeeping: the employer keeps the signed certificate on file in case of audit or state inquiry.

If you want the full end-to-end setup for multi-state hiring, registrations, notices workflow, and local tax handling, use these companion resources:

Reciprocity states in 2026

The table below lists common reciprocity relationships and the typical employee certificate form used to claim exemption. Always verify the latest form on the state tax agency site and keep a signed copy in your payroll records.

| Work state | Resident states that qualify for reciprocity | Typical nonresident certificate |

|---|---|---|

| Arizona | California, Indiana, Oregon, Virginia | WEC |

| District of Columbia | Any U.S. state other than DC | D-4A |

| Illinois | Iowa, Kentucky, Michigan, Wisconsin | IL-W-5-NR |

| Indiana | Kentucky, Michigan, Ohio, Pennsylvania, Wisconsin | WH-47 |

| Iowa | Illinois | 44-016 |

| Kentucky | Illinois, Indiana, Michigan, Ohio, Virginia, West Virginia, Wisconsin | 42A809 |

| Maryland | District of Columbia, Pennsylvania, Virginia, West Virginia | MW 507 |

| Michigan | Illinois, Indiana, Kentucky, Minnesota, Ohio, Wisconsin | MI-W4 |

| Minnesota | Michigan, North Dakota | MWR |

| Montana | North Dakota | MW-4 |

| New Jersey | Pennsylvania | NJ-165 |

| North Dakota | Minnesota, Montana | NDW-R |

| Ohio | Indiana, Kentucky, Michigan, Pennsylvania, West Virginia | IT-4NR |

| Pennsylvania | Indiana, Maryland, New Jersey, Ohio, Virginia, West Virginia | REV-419 |

| Virginia | District of Columbia, Kentucky, Maryland, Pennsylvania, West Virginia | VA-4 |

| West Virginia | Kentucky, Maryland, Ohio, Pennsylvania, Virginia | WV/IT-104 NR |

| Wisconsin | Illinois, Indiana, Kentucky, Michigan | W-220 |

Quick reality check: New York and New Jersey do not have reciprocity. A NJ resident working in NY generally pays NY as a nonresident and NJ as a resident (typically using a NJ credit for taxes paid to NY).

Payroll workflow for reciprocity cases

Capture the minimum facts

- Employee home address (resident state)

- Employee work address (work state)

- Work pattern (commuter, hybrid, remote, travel-heavy)

- Start date and payroll start date

Check if reciprocity applies

- Confirm whether the employee’s home state is listed as a reciprocal partner for the work state.

- If reciprocity does not apply, plan for standard nonresident/resident rules and consider whether your provider supports multi-state withholding cleanly.

Collect the nonresident certificate

- Have the employee complete and sign the correct certificate form.

- Store it in your payroll compliance folder (PDF scan is fine).

- Renew/update if the employee changes residence or work location.

Configure withholding correctly

- Withhold home state income tax.

- Set the work state income tax withholding to exempt (only if allowed under reciprocity and supported by your payroll system).

Do not confuse reciprocity with unemployment tax

- Reciprocity usually does not change SUI liability. SUI is commonly tied to the work state.

- If you are expanding into a new state, confirm employer registrations and notices handling before the first run.

Need the broader checklist for employer registrations and multi-state setup? Start here: Multi-State Payroll Setup Checklist (2026).

Common mistakes that trigger audits and employee frustration

- Not collecting the certificate: without it, the employer may be obligated to withhold in the work state.

- Assuming reciprocity covers local taxes: some local wage taxes can still apply even when state income tax reciprocity exists.

- Mixing up remote vs commuter rules: reciprocity helps commuters, but remote work can introduce other state rules and thresholds.

- No notices workflow: state letters and account issues become expensive when nobody owns them.

If you want a vendor shortlist that handles multi-state complexity better, see: Best Multi-State Payroll Companies (2026).

Recommended tools to keep multi-state payroll clean

Reciprocity issues usually show up when you’re scaling hiring across states. If you’re building your stack now, these starting points can help:

- Gusto for payroll + HR workflows in one platform

- Paylocity for unified HR + payroll automation at scale

- Best Payroll Companies in the USA for broader comparisons

FAQ

Do reciprocity agreements eliminate the need to file multiple state returns

Often they reduce filing complexity for wages by shifting withholding to the home state, but employees may still need to file depending on their overall situation (other income sources, partial-year residence, or incorrect withholding earlier in the year).

Does reciprocity apply to unemployment tax

Usually no. Reciprocity typically applies to state income tax withholding, while unemployment tax is commonly tied to the work state.

What if there is no reciprocity between the two states

In many cases, the employee will file a nonresident return in the work state and a resident return in the home state, usually using a resident-state credit for taxes paid to another state. Payroll withholding may need to follow the work state rules.

Is there reciprocity between New York and New Jersey

No. New York and New Jersey do not have a reciprocity agreement for state income tax withholding. A NJ resident working in NY generally pays NY tax as a nonresident and NJ tax as a resident, typically using NJ’s credit for taxes paid to NY.

:%20List%20of%20States,%20Forms%20&%20Payroll%20Withholding%20Rules){kind=link}